Divergence and Convergence in Emerging LPWAN Connectivity Protocols: Attitudes and Advantages

Comparing Emerging LPWAN Connectivity Protocols

In the continuing push for digitalization, IoT may no longer be a new concept but is still at the forefront of the enterprise push to future-proof designs, increase revenue, and decrease cost. Key in that decision-making process is selecting the right connectivity protocol. The number of available options has grown, and yet there is still no single one-size-fits-all solution.

An Omdia survey sponsored by Silicon Labs proves this out: on average, every enterprise is using 2-3 different technologies today, from cellular to Amazon Sidewalk, and Wi-Fi to Wi-SUN. That’s no surprise when every vertical and regional market brings its own unique characteristics, challenges, and types of enterprise to the table.

Download this whitepaper for an in-depth look at the established and emerging protocols driving LPWAN by protocol, specific regions, and markets.

Executive Summary

In the continuing push for digitalization, IoT may no longer be a new concept but is still at the forefront of the enterprise push to future-proof designs, increase revenue, and decrease cost. Key in that technological decision-making process is connectivity – and yet there is still no single one-sizefits-all solution.

Our Omdia survey proves this out: on average, every enterprise is using 2-3 different technologies today, from cellular to Amazon Sidewalk, and Wi-Fi to Wi-SUN. That’s no surprise when every vertical and regional market brings its own unique characteristics, challenges, and types of enterprise to the table. For example, utilities have large deployment sizes but very tight cost control, so easy integration is important. Or that deployments in India saw the biggest disruption from supply chain in recent years, pushing back ROI from investments and therefore heightening focus on quick deployments on future projects.

With so many competing challenges and technologies for connectivity, it’s no wonder that 1 in 4 enterprises still worry that they’ve made the wrong connectivity choice even on their existing deployments.

With so many competing challenges and technologies for connectivity, it’s no wonder that 1 in 4 enterprises still worry that they’ve made the wrong connectivity choice even on their existing deployments.

Sometimes though, that challenge is awareness – particularly as newer solutions come to market. For example, in a new Omdia survey, 39% of enterprises showed they aren’t aware of Wi-SUN and 45% not yet aware of Amazon Sidewalk, even despite strong use of Wi-SUN in Smart Cities/Utilities, and huge growth expected for Amazon Sidewalk in the next two years.

However, despite the ever-diverging aspects of IoT needs and solutions, some constants remain. The top two most important factors are performance and security – by a considerable margin, and even higher than cost. And for both the 1 in 4 who remain concerned on making the wrong choice and the 3 in 4 who are still using a changing mix of several technologies, having a trusted partner to support the journey is key in making the most from an enterprise IoT investment.

Introduction

Over the last decade, the number of IoT connectivity protocols and standards has grown continuously, with each standard featuring a different balance of speed, power, range, and capacity. Selecting the right protocol for a given application is one of the most important parts of designing an IoT installation, as a wrong decision early in the process can potentially limit the useable lifespan of an IoT network, or even limit its ultimate usefulness. For example, an industrial campus may have to choose between deploying a low-power standard like Bluetooth Low Energy (LE) in a mesh network, or a longer-range protocol like LoRaWAN. A network based on Bluetooth LE will have advantages in power, but will have a range measured in meters, meaning a mesh installation covering a large space will require a huge array of nodes to get coverage to the edge of the campus. Conversely, a LoRaWAN network will have no difficulty in covering a campus of several square kilometers but will be limited in throughput; if the data needs vary from the initial assumptions, or in the future change even slightly, the network may become unsuitable and require a costly refit.

Consequently, the increase in available protocols, both individually and in various combinations, means both opportunities and potential pitfalls for the network designer. Promising new connectivity standards may fail to gain traction because enterprises are unwilling to take a risk on an untested or unproven technology, choosing a more established standard that is less suited for the task. These decisions can also have long-term effects such as licensing, partnerships, and even engineering hires may be related to a single decision on connectivity. It is thus extremely important for all stakeholders in the process to examine not only what decisions on connectivity are being made, but how those decisions are being made, looking at who the key decision makers are, what influences they are under, and how they view their available set of options. Furthermore, it is important to examine how the effects of industry, geography, and scale might affect these choices, as no single solution at present would be appropriate in all settings, in all regions, and at all scales.

Selecting the right protocol for a given application is one of the most important parts of designing an IoT installation, as a wrong decision early in the process can potentially limit the useable lifespan of an IoT network, or even limit its ultimate usefulness.

Survey Overview

In January and February 2023, Omdia surveyed 451 respondents in three regions: North America (specifically the US and Canada), India, and Japan. Qualifying questions were asked, including the respondent’s role in the organization, their responsibility for decision making, and their organization’s revenue and IoT activity. Of the 451 respondents, a third had roles directly involved in or responsible for the selection of IoT connectivity. Specifically, 18% described themselves as ‘a decision-maker for IoT connectivity and technology decisions across the company’, while 7% said they were ‘a regional or divisional decision-maker for IoT connectivity and technology decisions’, and 4% each reported themselves as either ‘an implementer of IoT connectivity technology’ or ‘a key stakeholder in evaluating and selecting IoT connectivity technology’.

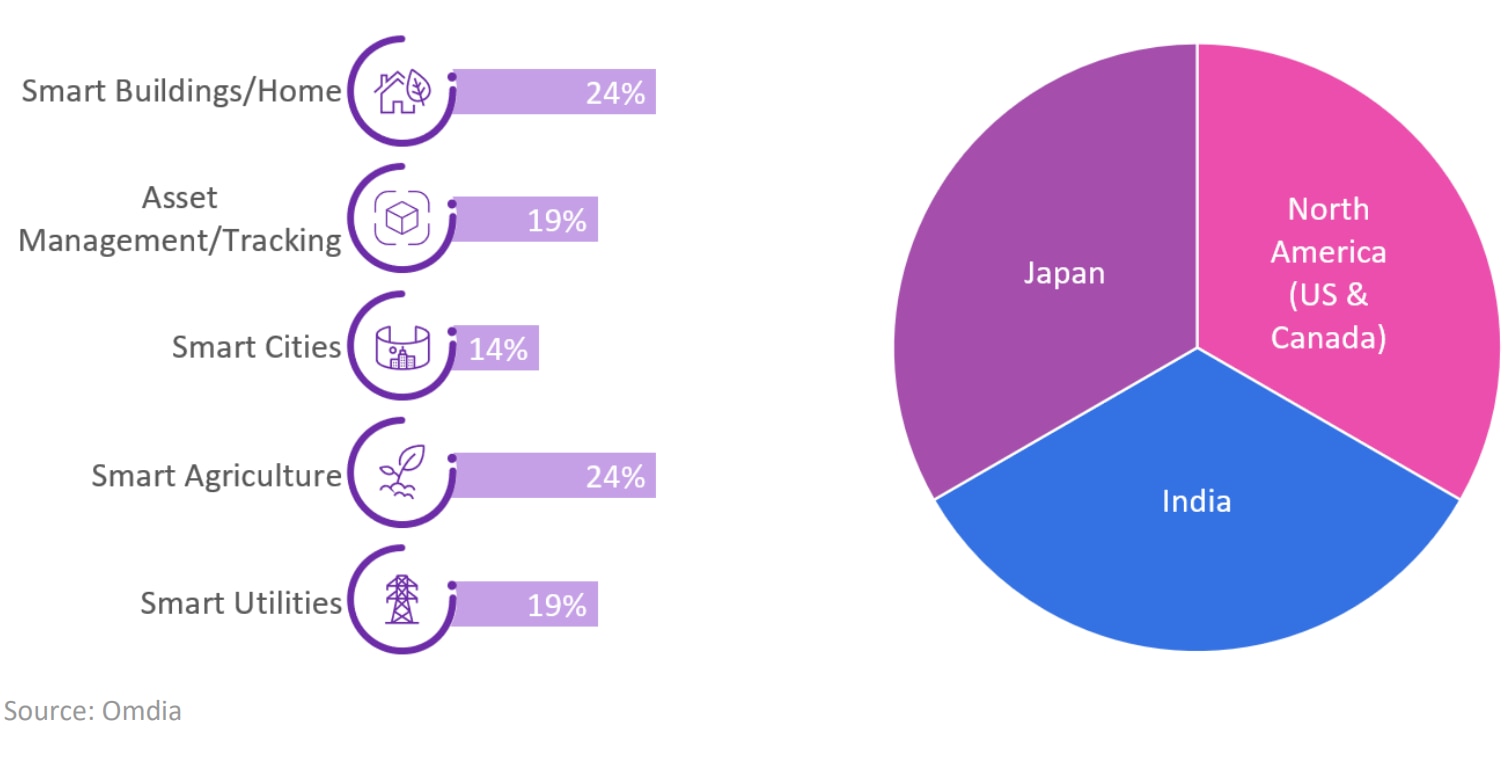

These respondents were then asked which of five major enterprise and commercial IoT applications their companies were involved in or were considering deploying. The largest share of respondents (27%) reported an interest or focus on smart buildings/smart home, while 25% had efforts in asset management and tracking. Sixteen percent each reported a focus on smart cities, smart agriculture, and smart utilities.

Figure 1. Survey Demographics

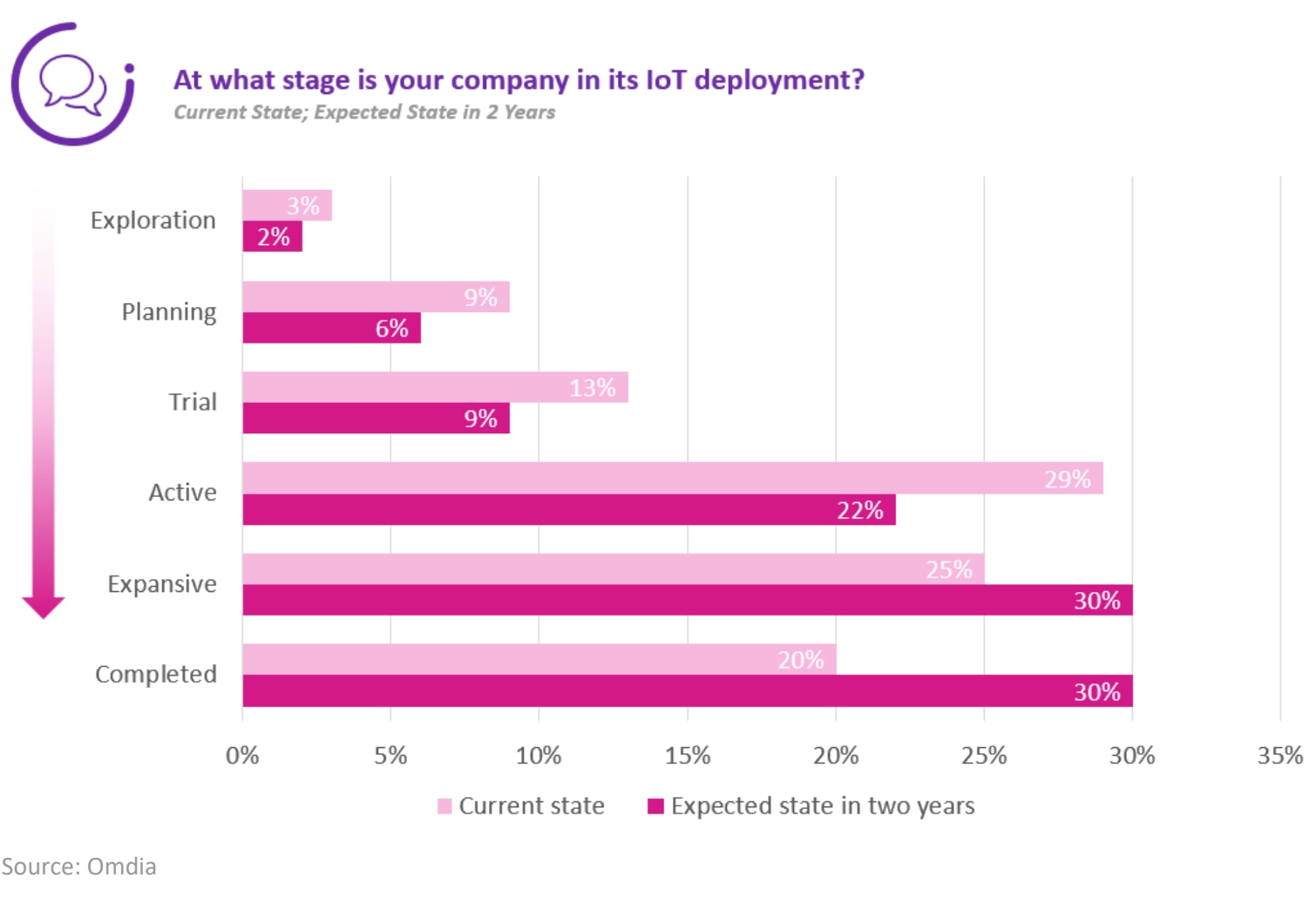

Respondents were asked to relate at what stage their company’s IoT deployment was currently, and at what stage they expected to be in two years’ time. For responses concerning the current state of IoT deployments, 29% reported their IoT offerings as being in an active state, defined as at least some IoT deployments in place and operational. Overall, nearly three quarters of respondents (74%) reported their companies had at least some active IoT installations, with 25% in an expansive state (leveraging existing IoT projects and infrastructure to address new use cases) and 20% at a completed stage, with all current plans for IoT fully implemented.

Figure 2. IoT Deployment Maturity

Looking ahead two years, 87% expect to have at least some active IoT deployments, with 60% of respondents moving into the two highest stages of deployment, an increase of 15 points over the 45% in 2022 who were in either expansive or completed phases. However, it is worth noting that 8% of respondents suggest that even in two years, they will not yet have reached even the trial stage, but rather will still be exploring a trial (2%) or planning a trial (6%).

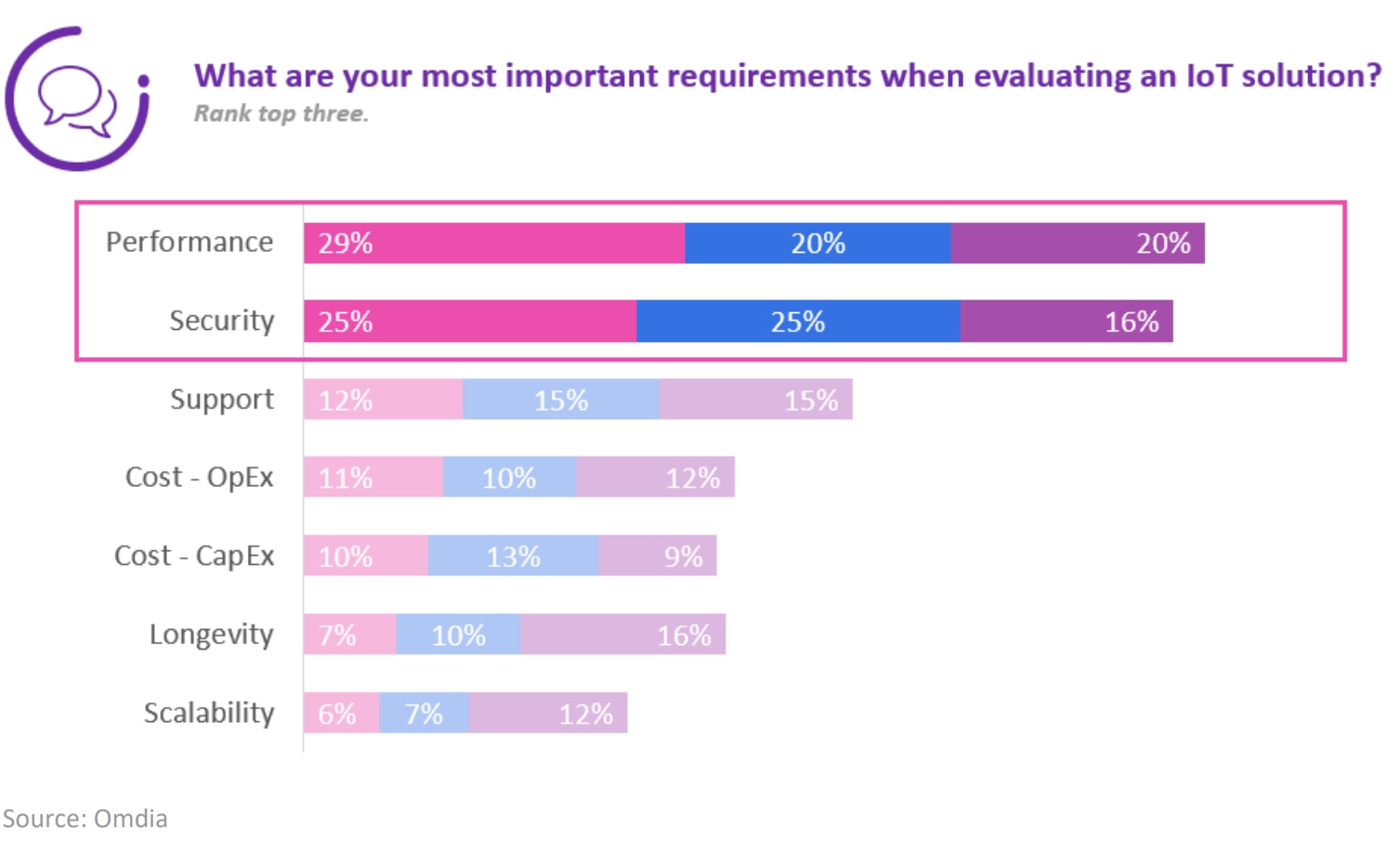

Respondents were also asked to rank their top three considerations when considering their IoT solutions. The seven criteria from which to select these three prime considerations included performance, security, support, cost (operating expenses), cost (capital expenses), longevity, and scalability. Overall performance and security were the clear priorities, with 69% of respondents ranking performance in their top three considerations (including 29% ranking it their first consideration) while 66% ranked security in their top three, with 25% ranking it their highest priority. Additionally, over half of respondents (54%) ranked either performance or security as their top priority when considering an IoT project.

Overall performance and security were the clear priorities, with 69% of respondents ranking performance in their top three considerations.

Support was a top-three consideration for 42% of respondents, while OpEx and CapEx costs were roughly even with longevity, with a third of respondents citing each of these as a top-three concern.

Finally a quarter said scalability was one of their three main considerations. 12% ranked support as their first consideration, and 27% said it was one of top first two considerations. Combining the two costs categories, 21% cited either OpEx or CapEx as their first consideration, meaning cost as a whole is clearly an important element of IoT installations.

Figure 3. Top IoT Solution Qualities

Detail by IoT Focus

If the responses are examined by main IoT activity, some differences are revealed:

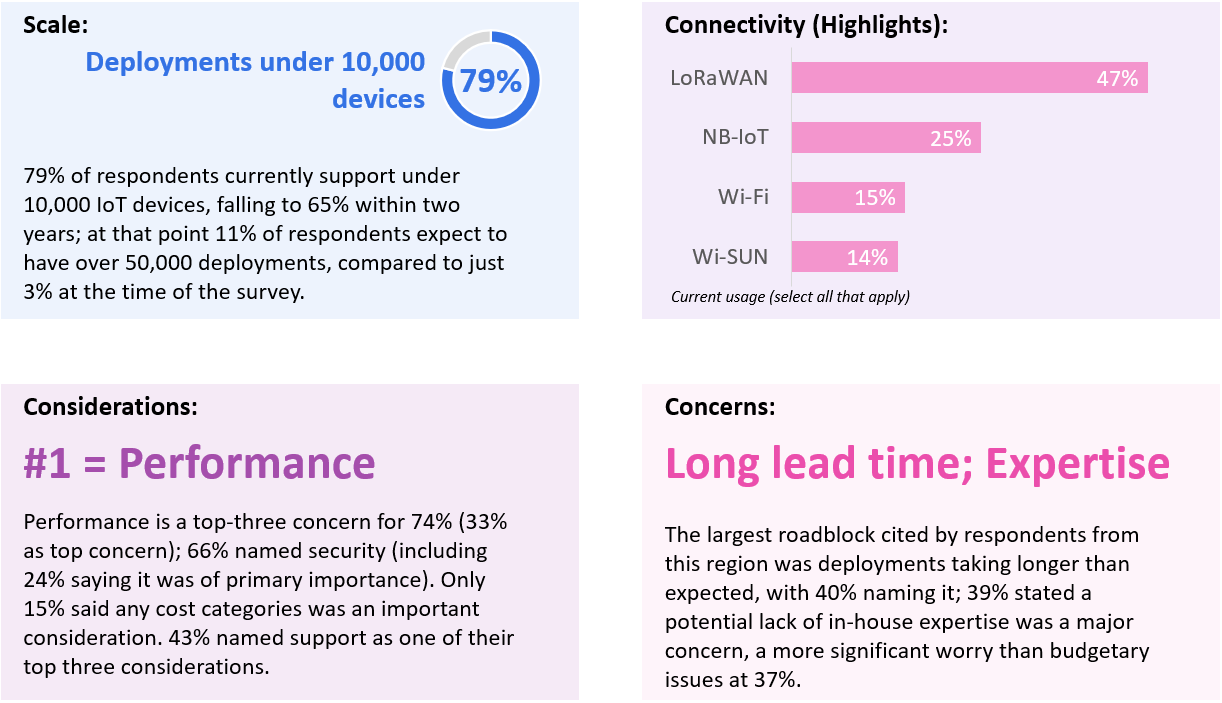

Asset Management and Tracking

Applications: Supply Chain (57%), Logistics (43%).

Summary: Supply chain/logistics applications are increasing adoption quickly, with medium-sized deployments. Only vertical to prioritize security over performance, with long lead times and in-house expertise as the top two challenges.

Smart Agriculture

Applications: Smart agriculture/farming (100%).

Summary: Typically the smallest deployment and business size, with low existing IoT knowledge and a natural cost cautiousness and preference for buying from a single partner/vendor. Expect use of Amazon Sidewalk to almost double in next two years, with awareness by far the biggest barrier.

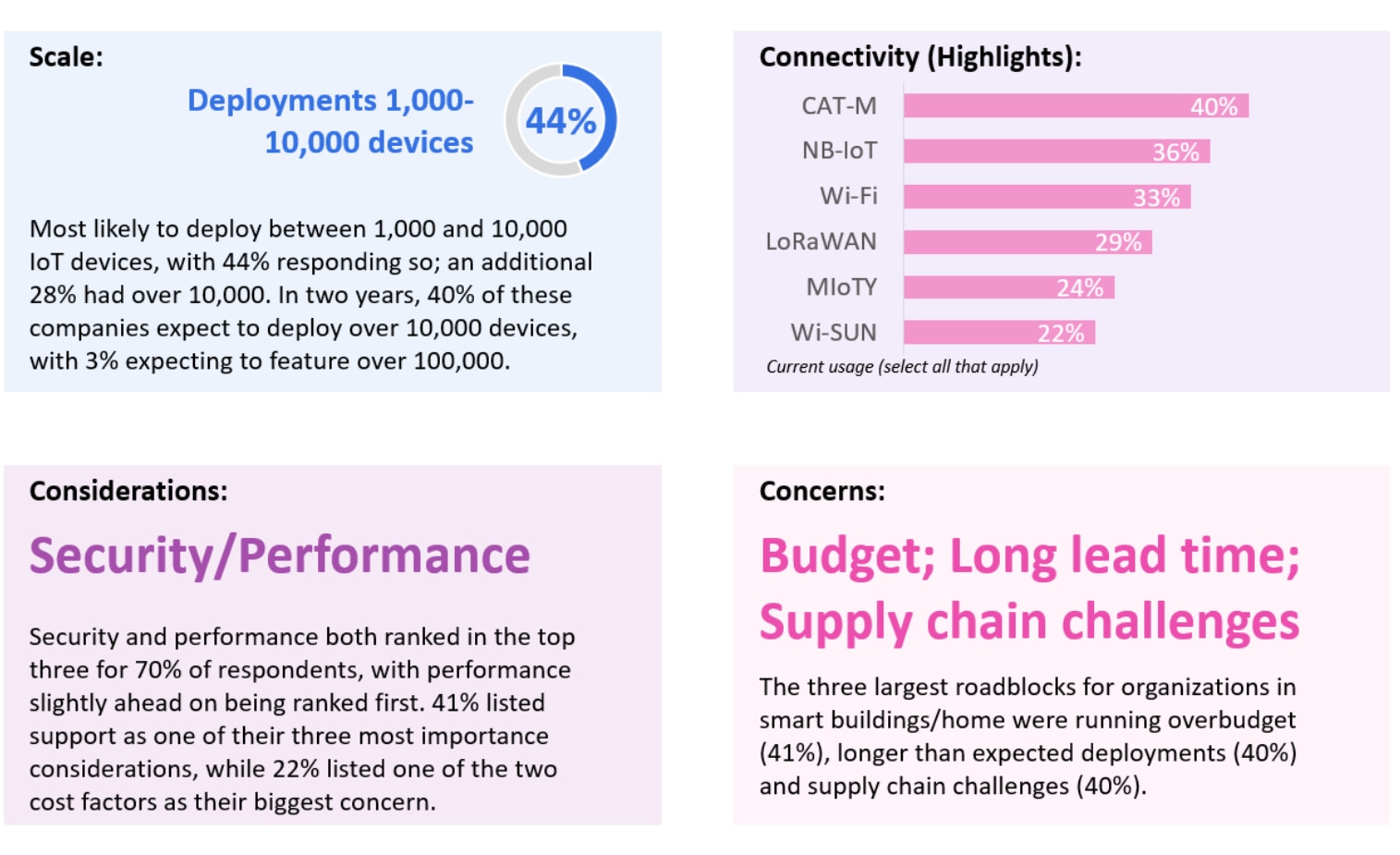

Smart Buildings

Applications: Security/Access (45%), Energy Management (36%), Building Traffic Management (19%).

Summary: Most challenged by supply chain, longer deployment time and being over budget. Strongest need for a developer/community support and an alliance-backed network. Biggest potential growth for Amazon Sidewalk in next two years of any vertical.

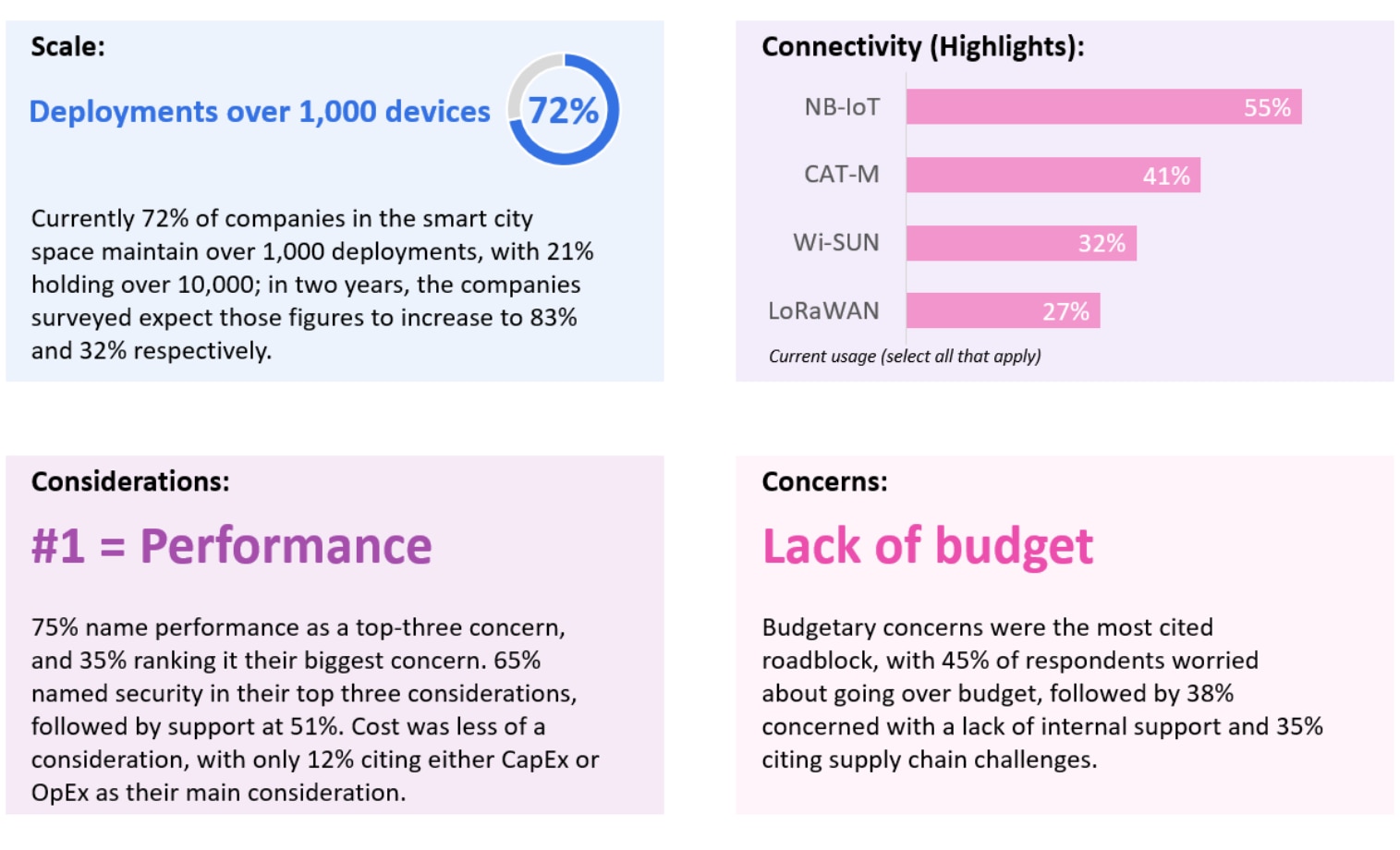

Smart Cities

Applications: Traffic Management (30%), Waste Management (30%), Smart Parking (20%), Smart Lighting (20%).

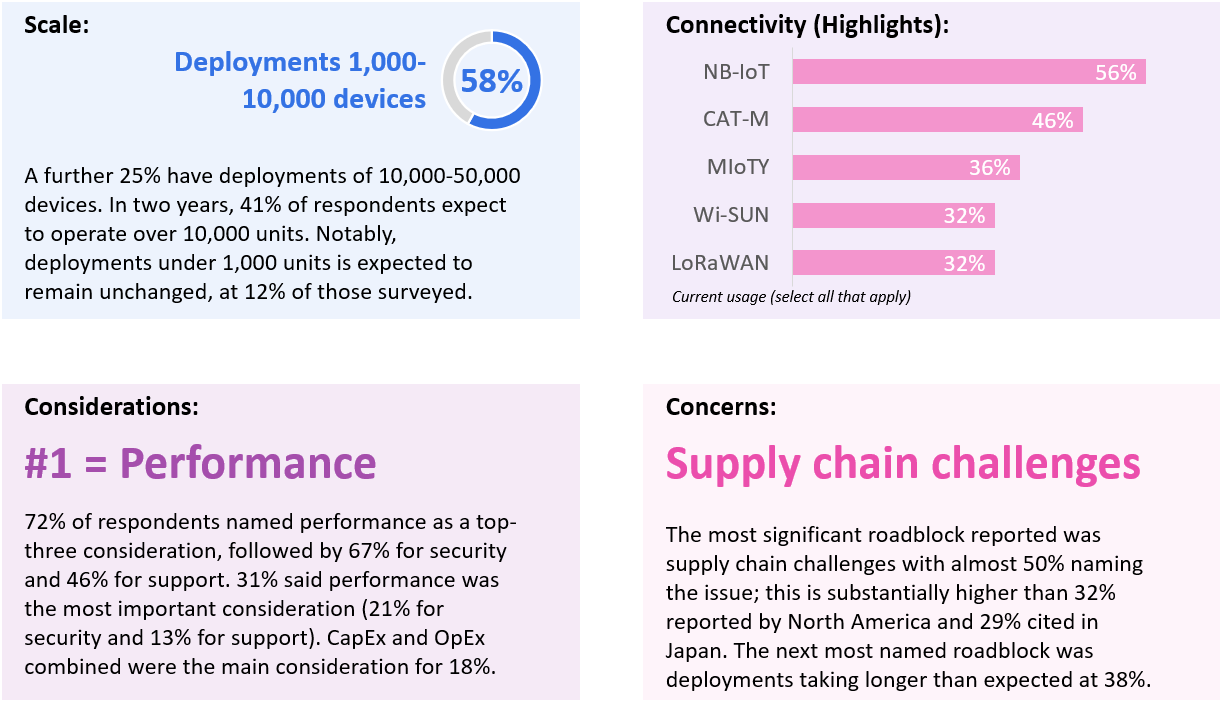

Summary: Still a relatively immature market despite some large deployments – smart cities have a big focus on performance and need longevity, but struggle on being over budget. Wi-SUN already the 3rd most used technology in this vertical.

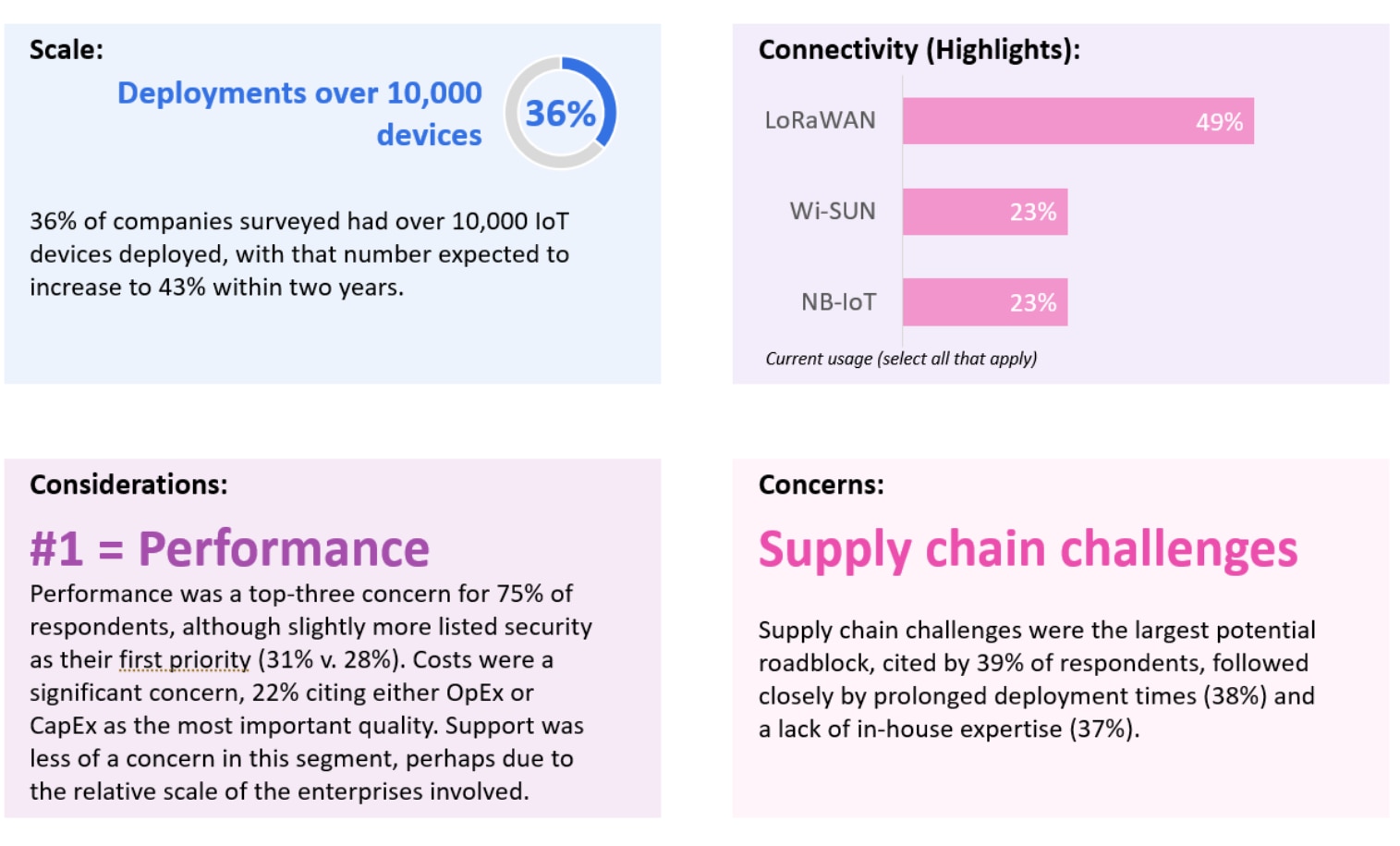

Smart Utilities

Applications: Energy/Utilities (44%), Distribution Automation (31%), Smart Metering (25%).

Summary: Smart utilities have some of the largest deployment sizes (by device count), but with tightly controlled costs/ability to spend and a need for integration with existing systems. Show strongest interest for any vertical in Amazon Sidewalk and Wi-SUN, the latter already the 2nd joint most used technology.

Regional difference

North America (US/Canada)

Top Application: Agriculture (17%), Supply Chain (13%), Logistics (12%), Energy (11%).

Summery: Performance focus even above security (e.g. ‘guaranteed uptime’), with high growth expected from the large number of smaller deployment projects seen to date. Relatively low awareness for Wi-SUN and higher awareness for Amazon Sidewalk, but strong need to see a developer network for technology.

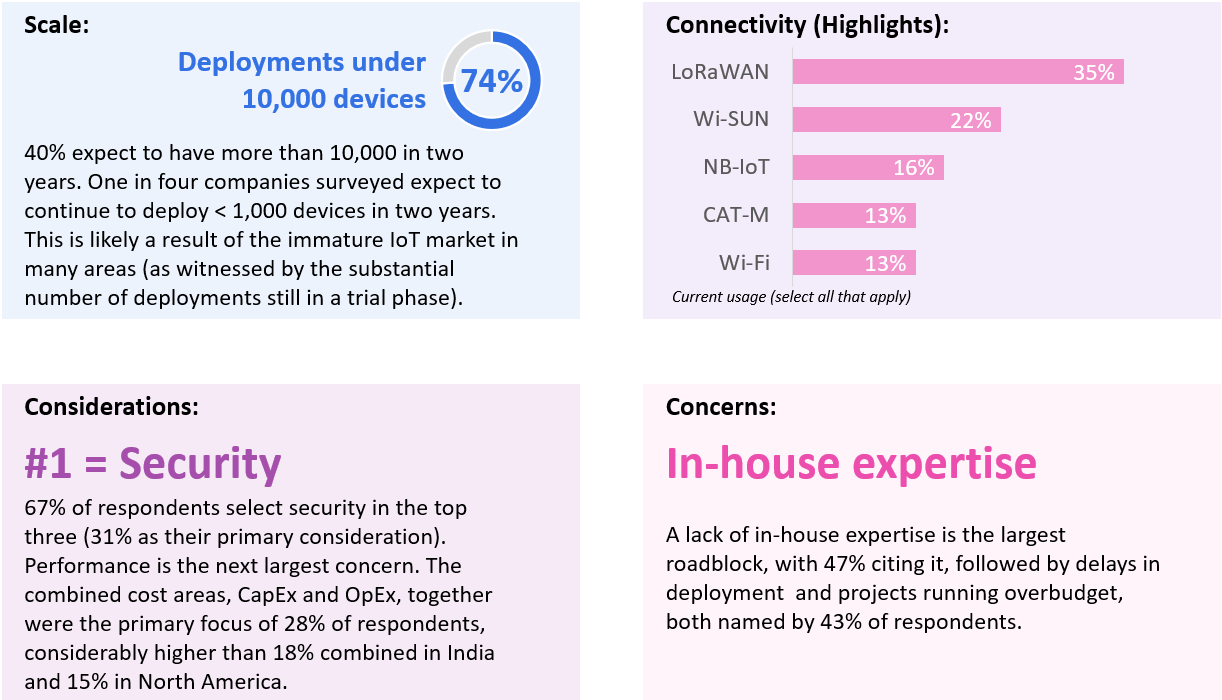

- Maturity: 74% of respondents from North America reported their IoT deployments were active, including 17% claiming all current plans for IoT installations were fully implemented; that figure was predicted to rise to 27% in two years, with 81% of respondents saying they expected at least some IoT deployments to be active at that time.

- Technology Considerations: When asked what performance or technical features are most needed in an IoT installation, 46% of North American respondents stated Integration/compatibility with current systems was a major concern, followed by 41% for guaranteed uptime.

- Support Needs: When discussing the most important criteria for support, respondents named strong developer networks and support as the most important feature overall, with 28% listing it as the highest priority and 67% listing it in their top three criteria. Availability of tools was the next most important consideration, with 20% citing it as their primary requirement and 62% putting it in their top three.

India

Top Applications: Supply Chain (21%), Security/Access (17%), Energy Management (14%).

Summary: The most bullish region on IoT deployment growth and with a relatively high average project size – also the most likely to buy end-to-end solutions but took a big hit in the supply chain disruption in recent years.

Japan

Top Applications: Agriculture (24%), Security/Access (11%), Logistics (10%).

Summary: The most security focused and cost conscious of the surveyed regions, with challenges around deployment integration and a lack of in-house expertise. Lowest current awareness level of any region for Wi-SUN.

- Maturity: 50% of companies surveyed stated their IoT deployments were active or expansive but not yet completed, although 19% said they expected all their planned IoT deployments to be complete in two years. 36% are currently in the process of planning or deploying a trial, compared to 20% in North America and 12% in India.

- Technology Considerations: Strong Developer Network/Community Support was the support criterion with the most naming it as a top-three consideration (63%), although the availability of tools had the largest number citing it as their main consideration, at 30%. 61% named tool availability as a topthree concern, with 58% mentioning ease of device certification.

- Support Needs: The most likely to partner with one or more vendors rather than build their own device hardware or software; respondents in India and North America were more than twice as likely to report building their own hardware and software.

Making the right choice

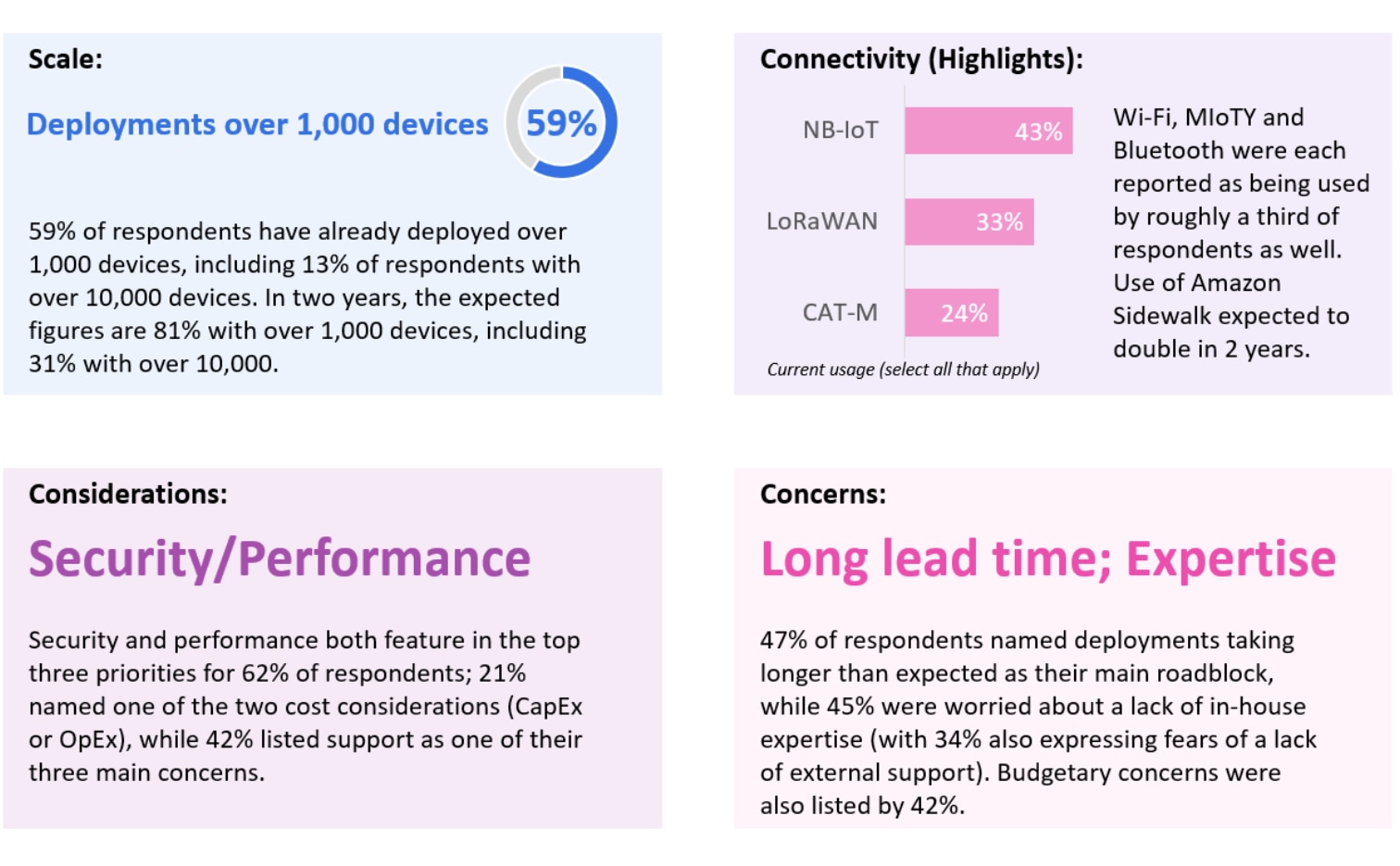

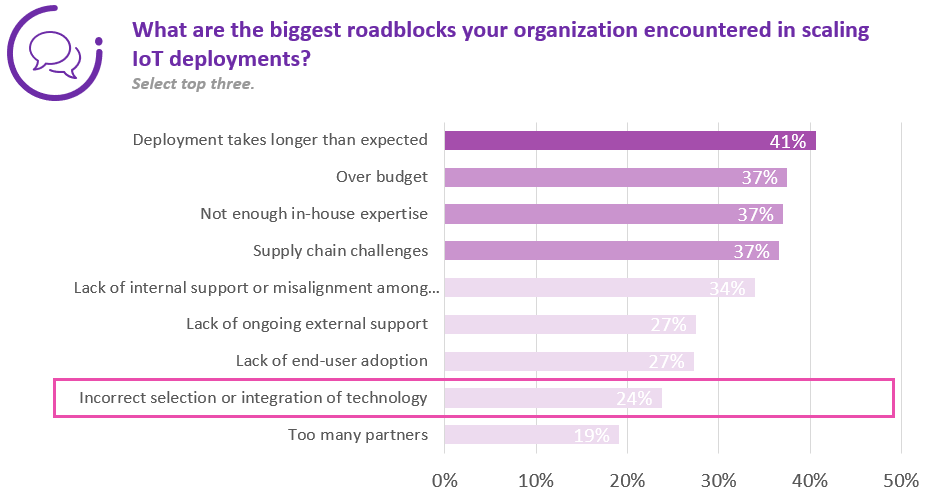

Looking at the responses as a whole, when asked what the biggest roadblocks encountered when scaling IoT deployments, the most commonly cited concerns were in many ways typical and although important fairly unexceptional. For example, deployments running behind schedule (41%) and over budget (37%), or difficulties in getting internal support or alignment behind priorities (34%), or the recently all-too-common supply chain difficulties (37%). However, one smaller area of concern is worth considering in some detail. 24% of respondents, or essentially one in four, has serious concerns about the incorrect selection or integration of technology. Furthermore, 27% worry about a lack of external support and 37% cite a potential lack of in-house expertise.

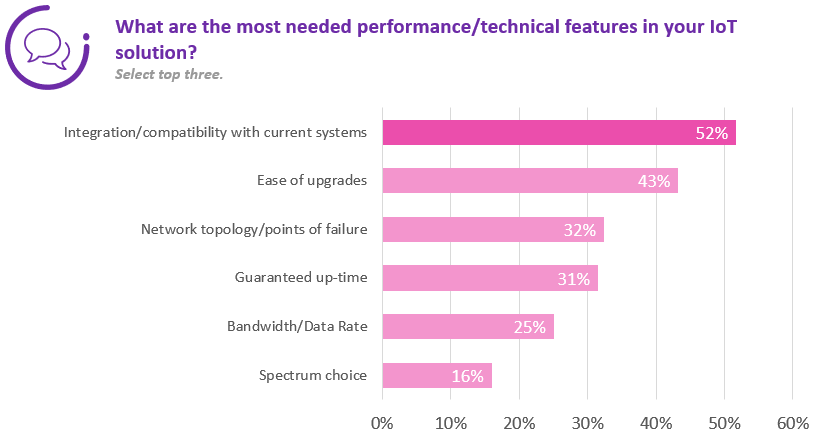

Additionally, when asked what performance or technical features were most important in an IoT solution, over half said that integration and compatibility with current systems was essential, significantly more than cited guaranteed uptime (31%) or bandwidth/data rate (25%). Thus, for over half of respondents, an absolutely essential feature, integration and compatibility, relies almost entirely on product or technology selection—an area where 25% are already worried about making the wrong choice.

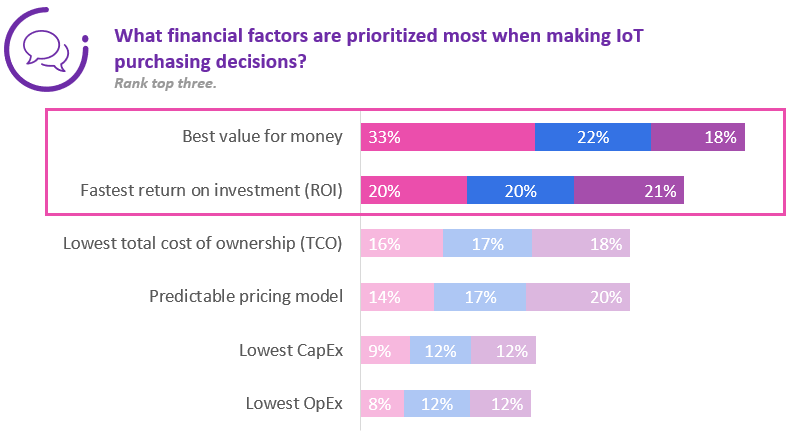

The wariness enterprises have over selecting the right technology and the requirement that it be easily integrated and compatible with current systems, is compounded by a need to minimize costs and maximize early returns on investment. When respondents were asked what financial factors were prioritized the most when making IoT purchase decisions, 72% named value for money as one of their top three considerations, while 61% reported fastest return on investment (ROI) as one of their three biggest concerns, with 20% citing it as their biggest consideration. This exacerbates the already significant pressure organizations feel over selecting the right technology and finding adequate support, since a path to ROI is expected quickly.

That is, a significant percentage of respondents, already facing pressure to produce a sufficient ROI, are also worrying about making the wrong choice of technology, in that they won’t be able to support themselves or get support to accomplish what they need the technology to do. That concern about making a wrong choice could potentially convince firms to choose what they regard as safe choices, opting for established or well-known solutions, rather than choosing ones best suited for their installation.

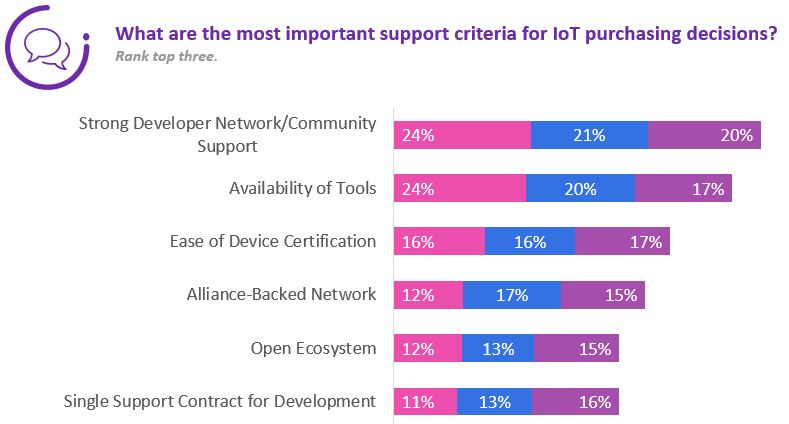

It is thus incumbent on vendors at every level to make sure there is overlapping support and advice available, so customers feel supported and understood in this process. It is also essential for new and emerging technologies to show the ways they enrich and expand the landscape. New does not need to mean risky or unproven, but customers need to know that the support they need and value they require is available. In fact, 65% of respondents, the largest number overall, list strong developer, network, and community support as a top-three consideration when considering the most important support criteria for IoT purchasing decisions, with 24% listing it as their highest priority.

As such addressing and alleviating these concerns must be seen as a critical part of the sales and delivery process by any vendor working in the IoT.

Examining Two Emerging Disruptors to IoT Connectivity

Looking more closely at attitudes to technologies in the IoT, attitudes toward and capabilities of two comparatively new forms of connectivity, Wi-SUN and Amazon Sidewalk, will be examined.

Wi-SUN

Wi-SUN, which originally stood for "Wireless Smart Utility Network” but has now been updated to “Wireless Smart Ubiquitous Network,” is an ultra-low-power and long-range sub-GHz mesh network designed primarily for smart city, smart utilities, and industrial IoT deployments. It is an open standard governed by the Wi-SUN Alliance. Wi-SUN offers higher throughput than both LoRaWAN and NB-IoT, as well as lower power consumption when in sleep mode; this means under the right circumstances, it can be more power-efficient than those two more commonly known long-range standards, as it can spend less time in transmit mode. With support for both IPv6 and its public key infrastructure (PKI), Wi-SUN also has some advantages in security, which as has been demonstrated is a consideration as important as performance for the great majority of respondents. The maximum transmission unit (MTU) of Wi-SUN is just over 1200 bytes, with a transition rate of 50 kbps to 2.4 Mbps. This is notably lower latency than LoRaWAN, which has an upper limit of roughly 60 kbps, while NB-IoT tops out at 140 kbps (uplink). As such Wi-SUN is optimised for short bursts of information, sent with minimal latency and with high security.

Amazon Sidewalk

Amazon Sidewalk is a low-bandwidth, long-range protocol which uses the existing array of Amazon smart home devices to provide an extended IoT network, with some Ring devices and Echo speakers acting as access points, thus creating an ad-hoc network. Amazon Sidewalk uses a combination of Bluetooth LE for short-range connectivity in the home, and sub-GHz, including FSK and CSS modulations for long-range, area neighborhood networks. Amazon device owners agree by default to share a small portion of their internet bandwidth with the network, up to pre-set limits, with the understanding that they will also benefit from this sharing. Amazon device owners share some of their internet bandwidth with the network, up to pre-set limits, with the understanding that they will also benefit from this sharing. For example, in the event of a power loss, a Ring camera will still be able to upload notifications by making use of an online Amazon Sidewalk connection, while device trackers such as Tile can also use the network, which makes finding devices equipped with the tags easier. Amazon Sidewalk is also integrated with AWS’s IoT Core service, meaning developers have access to the network as part of their IoT Core subscription.

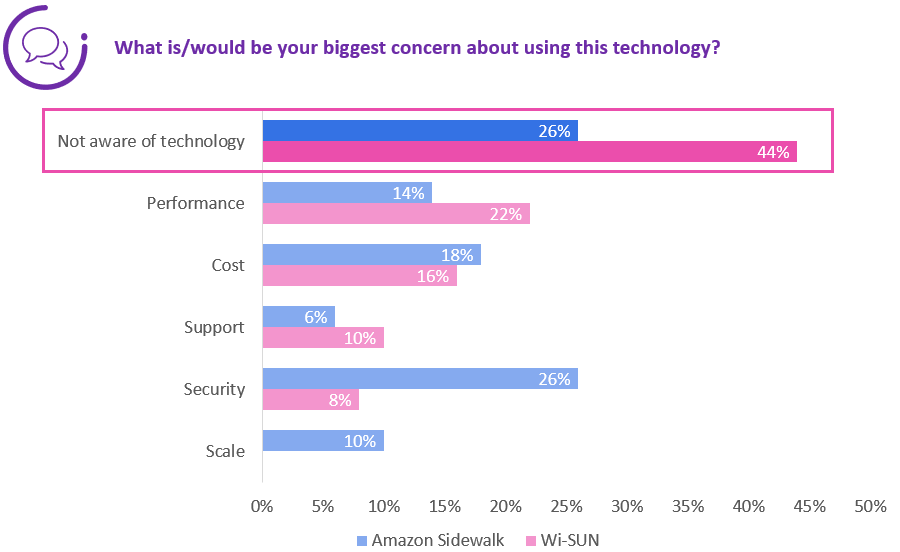

Lack of Awareness is the Biggest Concern

Overall respondents were less aware of Wi-SUN and Amazon Sidewalk than they were of moreestablished protocols. 39% said they were not aware of Wi-SUN and 45% said they were not awareof Amazon Sidewalk. That lack of awareness is clearly the most significant concern about both technologies.

For example, among respondents focused on Smart Utilities, Wi-SUN is the second most commonly used technology, tied with NB-IoT at 35% and behind LoRaWAN with 40%. Clearly as Wi-SUN was designed for and is most used in the utilities segment, it has more recognition and consequently more use. Wi-SUN has also become a significant technology in the Smart City space, with 32% of respondents focused on that segment reporting using Wi-SUN, behind NB-IoT (55%) and CAT-M (41%) but ahead of LoRaWAN (27%).

Looking ahead, both Wi-SUN and Amazon Sidewalk are technologies enterprises are demonstrating active plans for the near future. When asked what technologies they plan on actively incorporating into their IoT solutions within the next two years, 23% plan on using Wi-SUN and 19% of respondents name Amazon Sidewalk— this would represent tremendous growth for Amazon Sidewalk, especially considering it was only opened to developers in 2023. 29% of respondents in Smart Agriculture plan on using Wi-SUN, while 21% of those surveyed with a focus on asset management and tracking plan on using Amazon Sidewalk. However, while that was the highest response from a vertical, it is notable that there was enthusiasm for Amazon Sidewalk in all five verticals surveyed, with no vertical expecting to see use below 15% for Amazon Sidewalk in two years. Considering the previously noted lack of awareness of Amazon Sidewalk, reaching 45%, this indicated that Amazon Sidewalk is rapidly becoming a preferred solution among those with substantial awareness of the technology.

Case Study: Wi-SUN

At the International Institute of InformationTechnology in Hyderabad, India (IIIT-H), and fundedby the government of India, the Center of Excellenceon IoT for Smart Cities has established a Smart CityLiving Lab on campus which duplicates a typicalurban environment to allow for research andexperimentation in technologies that can promotesocial, economic, and environmental quality of life. Acampus-wide network of Wi-SUN nodes offers controlover individual streetlights based on weatherconditions, with light poles fitted with router nodesacting as the network’s control and backbone. Anarray of sensors, both line-powered and batterypowered, are connected as end nodes, forming arobust Wi-SUN mesh. This dense network ofstationary nodes is essential to enable thedeployment and demonstration of Wi-SUN beyondsimple applications like streetlights. The capability ofWi-SUN to deploy in this mesh pattern, as opposed tothe star topology typically used by LoRaWAN and NBIoT as well as CAT-M, is a particular point in Wi-SUN’sfavour in the Smart City space.

Case Study: Amazon Sidewalk

New Cosmos, a long-established maker of residential natural gas alarms, used Amazon Sidewalk as their connectivity choice for their line of DeNova Detect wireless alarms. The design uses microelectromechanical system (MEMS) sensors for gas leak detection as well as Amazon Sidewalk, suing its combination of Bluetooth LE and LoRaWAN to minimize power consumption and maximize battery life, as well as using the de facto mesh network created in residential neighborhoods to ensure always-on connectivity. This means the device can operate independently for a number of years without requiring a battery change. The technology supports security features regarded as essential for the application, such as multilayer encryption. A partnership with Silicon Labs ensured access to all tools and support necessary.

Conclusions

While other aspects are certainly increasing in importance, technology performance and security are without question the most important considerations by those surveyed. This means every firm engaged in designing, manufacturing, and supplying connectivity hardware should make it transparent how their security is offered, how it works, how it scales, and how it integrates. As we have seen with the lack of awareness affecting newer technologies, it is especially incumbent on those promoting these newer technologies to lay out their security proposition for the world.

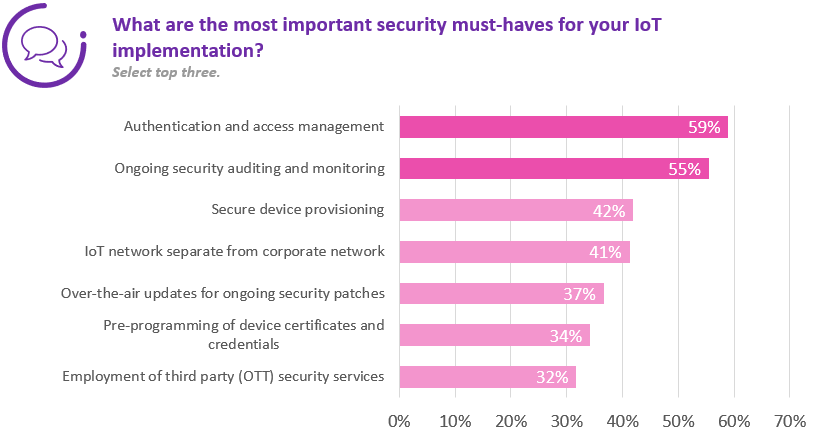

For example, Amazon Sidewalk and Wi-SUN both tick virtually every box of security requirements, with robust authentication, secure access management, multiple secure layers of encryption, secured provisioning and OTA updates. Those supplying these devices should go further in allying any lingering concerns about security, as the lack of awareness could potentially breed mistrust.

Respondents show that the more aware they are both of Wi-SUN and Amazon Sidewalk, the more likely they are to feel positively towards both technologies. When respondents were asked to give detail of their awareness of Wi-SUN, the 39% awareness was segmented into 11% who were not aware at all and 27% who were aware but did not know enough to make a decision (with 1% lost due to rounding). Of the remaining 62%, 10% said they were aware and using the standard, while 29% said they were aware and would consider using it. That translates to a positive attitude towards Wi-SUN from 63% of those aware of the protocol. Similarly, for Amazon Sidewalk, 65% of those with enough awareness of the protocol shared a positive attitude toward the protocol. As such, cutting through the lack of awareness is an obvious but still important step in fostering its growth.

Amazon Sidewalk and Wi-SUN both tick virtually every box of security supplying …Those these devices should go further in allying any lingering concerns about security, as the lack of could awareness potentially breed mistrust.